As the birthdays go by, the urgency to prepare seriously for your retirement grows. One vital aspect of this is ensuring your retirement fund is in good shape. However, the Singapore Management University’s Centre for Research on Successful Ageing (ROSA) discovered that only 34% of Singaporeans believed they were well-prepared for retirement.

Preserving your wealth before you stop working allows you to enjoy your ideal retirement lifestyle. Remember, when you retire, your salary comes to a halt too. You might have other income streams right now and intend to keep them while you’re retired, but this is still a sizable amount of money per month which stops coming in.

Fortunately, there are ways you can protect your wealth before swapping the daily 9-5 and monthly paycheck for several decades of worry-free living. Continue reading to learn more about all five of them.

1. Bolster Your Upcoming CPF LIFE Payouts

CPF LIFE is a lifelong annuity plan activated once you’re anywhere from 65 to 70 years old, depending on the payout age you select. This scheme from the CPF Board ensures you receive monthly payments based on the amount in your CPF Retirement Account (CPF-RA).

When you voluntarily fund your CPF-RA before you retire, it increases your monthly CPF-LIFE payouts down the road.

Also, you protect your wealth in two additional ways:

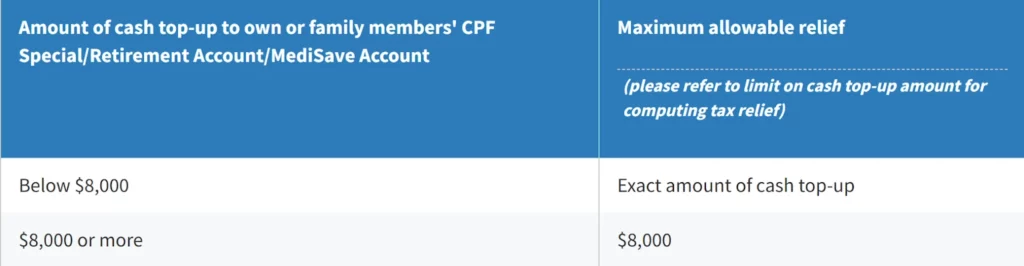

Extra Income Tax Reliefs

Source: Inland Revenue Authority of Singapore

For every income tax assessment year, you can enjoy up to S$8,000 more in reliefs by funding your CPF-RA, among other accounts. As mentioned above, growing your CPF-RA leads to increased CPF-LIFE payouts when you retire. You may not be able to access the money right now, but it definitely beats forking out more for income tax.

A Shield From Inflation

Directing funds to your CPF-RA also means the money works harder for you. That’s because the CPF-RA currently yields 4% p.a. in interest. Like the rest of your CPF accounts, your funds aren’t sitting idle. The interest they earn protects you from inflation and prevents their value from eroding as much as possible.

Related: An Essential Guide to Calculating Your CPF LIFE Payouts

2. Lower the Risk Level of Your Investment Portfolio

As you grow older, your personal investment horizon shortens because your lifespan shrinks. This weakens your portfolio’s ability to heal from market downturns because by a certain age, you literally cannot wait until it recovers before liquidating it. Therefore, you need to safeguard your wealth by periodically adjusting your portfolio’s asset allocation.

Here’s an example of how this looks like if you have a portfolio containing only the three traditional asset classes.

| Equities | Fixed Income | Cash Equivalents Assets | |

| 30 Years Old | 80-90% | 10-20% | 0% |

| 50 Years Old | 60-70% | 30-35% | 5-10% |

| 70 Years Old | 40-50% | 40-50% | 10-20% |

A rule of thumb which has stood the test of time and was even updated recently would be this: Allocate a percentage of your portfolio to equities equal to 120/110 minus your age.

Assume you’re 30 years old now. Based on the principle above, equities should comprise 80-90% of your investment portfolio (i.e. 120 – 30 and 110 – 30). The remaining allocation should be set aside for fixed income instruments like investment-grade bonds and money market funds.

This means that by 70 years old, it’s ideal to liquidate approximately 50% of your equities. You should then re-invest the capital in fixed income assets. A small portion can be directed to assets such as short-term government bonds and commercial paper.

Stocks can earn the greatest returns among the three asset classes showcased above. However, the equities asset class is also the group’s riskiest one. Don’t jeopardise your retirement fund just for a few percentage points extra in projected returns.

Related: How to Rebalance Your Investment Portfolio When Bond Prices Fall

3. Set Up Passive Income Streams

The term “passive income” is fairly self-explanatory. It’s a sum of money which comes in regularly without a lot of manual interference after your initial investment is made. Several examples include renting out your apartment and collecting dividends from the shares you hold.

When you create a passive income stream, you’re protecting your wealth in two ways:

- Your capital benefits from the investment’s value potentially rising over time, along with the steady payouts you receive. You can re-invest the funds or use the money for your daily expenses in retirement.

- You’re hedging yourself against inflation, especially once retirement comes along. When you have a passive income stream, it ensures the value of your money is preserved. Being able to comfortably afford your daily expenses when you’re not actively drawing a paycheck any more will give anyone peace of mind.

In Singapore, dividends from shares are an especially attractive passive income stream because you don’t have to pay taxes for the most part. The only dividends you need to pay taxes for are from co-operatives (NTUC Healthcare Co-operative Ltd, MCCY Registry of Co-operative Societies, etc.), foreign dividends you receive specifically via a partnership in Singapore, and income distribution from Real Estate Investment Trusts (REITs).

Related: How to Pick Dividend Stocks For Your Investment Portfolio

4. Stay Abreast of Scams and Fraud

This method isn’t a direct way to preserve your retirement fund’s value or grow your wealth, but it’s important to learn about nonetheless. The tactics criminals use for financial scams today are sophisticated, and will only become more refined as the years go by.

When you know about the latest scams being used to syphon money off unsuspecting individuals, you can keep your wealth intact to the best of your ability.

Here are some best security practices to follow:

- Don’t share your bank account PIN or investment platform password with anyone

- Keep your personal details private, including your NRIC number. Should an organisation’s staff require your NRIC number for verification, they should only ask for a partial version of it.

- If someone claiming to be a person you know asks for money, check their claim by giving them a call or insisting to meet in person.

- Don’t prepay for an item or service by purchasing a gift card. If a seller or service provider asks for this, ignore them and immediately seek an alternative option.

In short, whenever your instincts are telling you something’s not right, you’d do well to listen to them and be extra cautious. This will save you from many a sleepless night trying to recover the retirement fund you worked and invested so hard for.

5. Think About Your Healthcare Costs

Getting older comes with an increased risk for multiple health conditions, from Alzheimer’s disease to cancer. This leads to potentially higher healthcare costs, which drives home the idea that health is wealth. When you’re aware of the healthcare costs you might incur after retirement, it allows you to have the right insurance policies in place.

By doing this, you’re safeguarding your wealth as you can deflect a significant portion of medical expenses away from your retirement fund. Singaporeans have access to the MediSave, MediShield Life, and CareShield Life schemes, but you’ll need to consider if these are enough for your medical expenses in retirement.

For one, you may want to upgrade your Integrated Shield Plan or just drop the idea to cancel it upon retirement. At first glance, this doesn’t protect your wealth because of the higher premiums. However, if you believe older you will require specialised care in a Class B1 or A ward should you be hospitalised, it’s better than paying for the costs out of pocket.

Secondly, consider beefing up your basic CareShield Life/Eldershield plan with a Supplement. For CareShield Life, the base plan pays out just S$600 per month when you’re disabled. Adding a Supplement definitely means higher premiums, but your monthly payouts will increase significantly and you gain access to other benefits too.

Related: How CareShield Life Might Just Save You and Your Family, Regardless of Age

In Closing

As retirement draws close, the need to protect and preserve your wealth is at its highest. For most of us, our retirement fund represents the final largest expense that we need to save up and invest for. Once you’re in the home stretch, you’ll have to ensure that this fund stays intact, whether by managing your healthcare costs or hedging it against inflation.

The methods discussed above are just several ways which you can protect your wealth when retirement approaches. Others do exist, but they all follow the core principle of minimising the risk you take on when investing in your later years, and making sure your money can keep up with the pace of inflation.

Read More:

- Guide To Retirement Planning in Singapore

- How Do You Determine the Investment Horizon For Your Assets?

- Five Ways to Earn Passive Income in Singapore

- How to Plan Your Finances for Short, Medium and Long Term Goals

- How to Start Planning For Retirement in Your 20s and 30s

Cover image source: Unsplash

Enquire more and contact us today!

Want to know more about AMTD PolicyPal Group insurance plans?

Cannot find what you are looking for? Please reach out to us at Contact AMTD PolicyPal

Disclaimer: This content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation or endorsement by AMTD PolicyPal Group in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Under AMTD Digital, AMTD PolicyPal Group is a leading Singapore-based FinTech company. AMTD PolicyPal Group consists of: PolicyPal Pte. Ltd., Baoxianbaobao Pte. Ltd., PolicyPal Tech Pte. Ltd., and ValueChampion